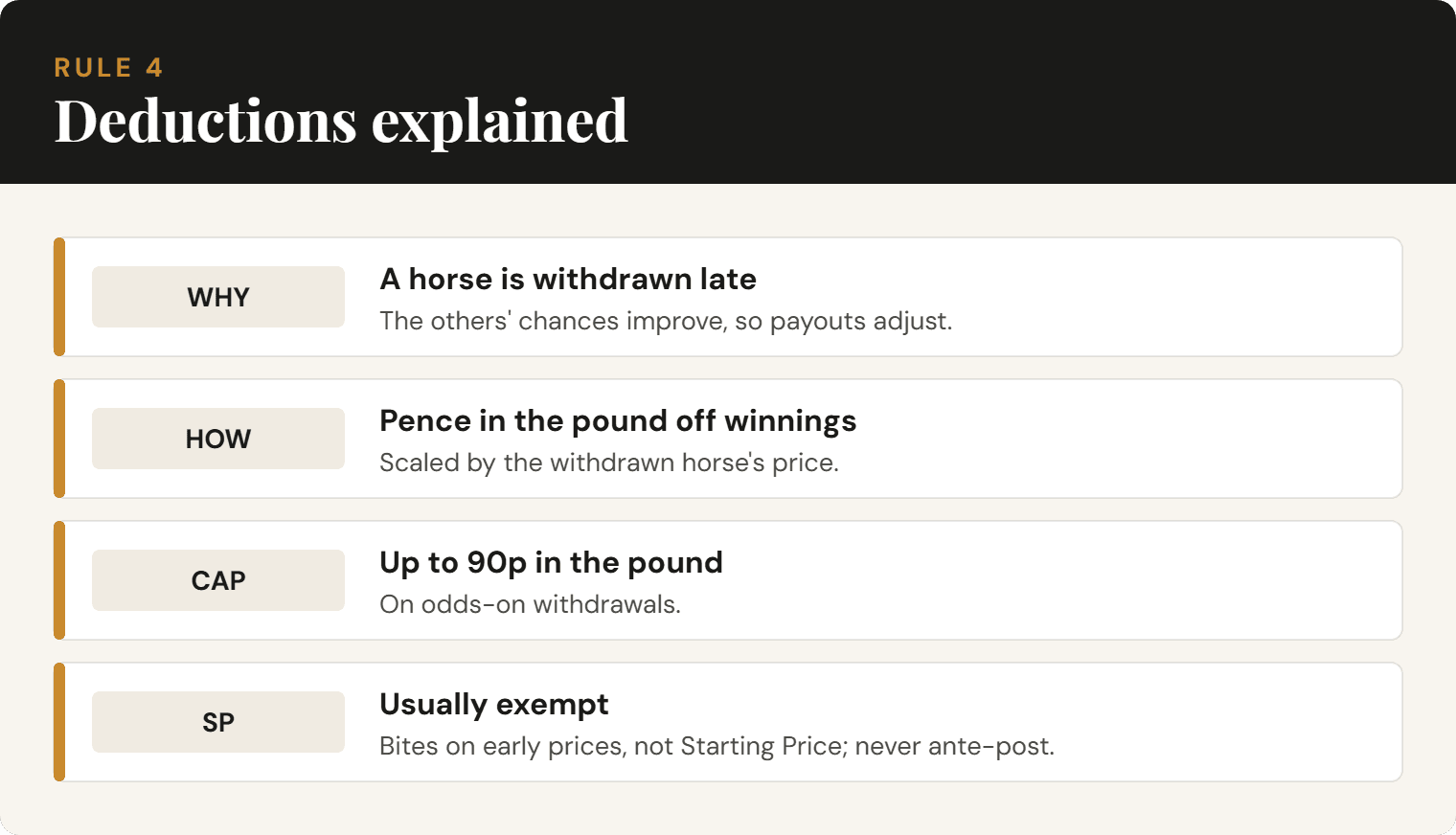

Rule 4 Deductions Explained

● FormDialHorse RacingRule 4 is the mechanism bookmakers use to adjust payouts when a horse is withdrawn from a race after the market has formed. When a runner is removed, the remaining horses all become more likely to win — but the odds on your bet were set when the full field was intact. Rule 4 corrects for this by applying a deduction to your winnings. The deduction is not arbitrary. It is set by the Tattersalls Committee, applied uniformly across UK bookmakers, and calculated from the price of the withdrawn horse at the time of withdrawal.

How the Deduction Is Calculated

The deduction is a percentage taken from your winnings — not from your stake. It is applied after the race, to the profit element of your return. The percentage is determined by the price of the non-runner at the time it was withdrawn — the shorter that price, the larger the deduction, because removing a strong fancy distorts the race far more than removing an outsider.

| Price of Non-Runner | Deduction |

|---|---|

| 1/9 or shorter | 90p in the £ |

| 2/11 to 2/17 | 85p in the £ |

| 1/4 to 1/5 | 80p in the £ |

| 3/10 to 2/7 | 75p in the £ |

| 2/5 to 1/3 | 70p in the £ |

| 8/15 to 4/9 | 65p in the £ |

| 8/13 to 4/7 | 60p in the £ |

| 4/5 to 4/6 | 55p in the £ |

| 20/21 to 5/6 | 50p in the £ |

| Evens to 6/5 | 45p in the £ |

| 5/4 to 6/4 | 40p in the £ |

| 8/5 to 7/4 | 35p in the £ |

| 9/5 to 9/4 | 30p in the £ |

| 12/5 to 3/1 | 25p in the £ |

| 16/5 to 4/1 | 20p in the £ |

| 9/2 to 11/2 | 15p in the £ |

| 6/1 to 9/1 | 10p in the £ |

| 10/1 to 14/1 | 5p in the £ |

| Over 14/1 | No deduction |

A Worked Example

The arithmetic is simpler than the scale makes it look. Work it in three steps — figure the profit, take the deduction off that profit, then add the stake back.

The same logic scales to any price. A shorter non-runner means a bigger slice off the profit; an outsider above 14/1 means none at all. To run your own numbers without the mental arithmetic, the Bet Calculator applies the correct band to singles, each-way bets and multiples. If you are still getting to grips with how 4/1 or 2/1 translate into returns, Betting Odds Explained covers the fractions.

When Rule 4 Applies

Rule 4 applies whenever a horse is withdrawn after the final declaration stage and the bookmaker has already priced the market. The most common triggers are late veterinary withdrawals, going-related withdrawals on the morning of the race, and horses that refuse to enter the stalls at the start. For the wider rules around withdrawn runners and refunded stakes, see Non-Runner Rules Explained.

Does It Apply to My Bet?

This is the question that catches most punters out, and the answer turns on which price you took.

Early (board) price

- AffectedYes — Rule 4 bites. You locked in a price set against the full field, so the deduction corrects for the missing runner.

- ExamplesFixed-odds and board prices taken in the minutes or hours before the off.

Starting Price (SP)

- AffectedGenerally no — the SP is struck after withdrawals, so it already reflects the reduced field. No separate deduction is made.

- ExceptionA withdrawal so late that no fresh market can form — for example a horse refusing to enter the stalls — can still carry a deduction on SP bets.

Rule 4 also does not apply to ante-post bets. If you backed a horse weeks out and a different runner is later withdrawn, your bet stands at the original price with no deduction — one of the genuine edges of betting early, covered in Ante-Post Betting Explained.

Multiple Withdrawals

If more than one horse is withdrawn, the deductions are cumulative — the individual figures are simply added together. Two non-runners carrying deductions of 25p and 15p combine to 40p in the £. The Tattersalls rules cap the total at 90p, so no matter how many short-priced runners come out of the same race, you always keep at least 10p of every winning pound.

Reaching the 90p Cap

Reaching that ceiling takes genuinely short prices, not merely two market leaders. An odds-on favourite withdrawn (90p) hits the cap on its own; a 5/4 leader (40p) plus a 7/4 second favourite (35p) combine to 75p in the £. Either way the bulk of your winnings is gone even on a successful bet, so if you see multiple late withdrawals, recalculate your expected return before deciding whether the bet still holds value.

Rule 4 deductions are one of the hidden costs of betting that most punters never account for. Over a season they erode returns systematically — particularly on days of changeable weather, when going-related withdrawals are common. The practical defence is simple: on days when non-runners look likely, take SP rather than an early price. The SP is settled after all withdrawals, so it absorbs them without a separate deduction. The trade-off is that you give up the chance to lock in a bigger board price — but on a doubtful day, that is often the better bargain.

Common Questions

From your winnings only. Your stake is always returned in full on a winning bet — the deduction applies to the profit element, scaled by the withdrawn horse’s price.

Generally no. The starting price is struck after withdrawals, so it already reflects the smaller field and no separate deduction is made. The one exception is a withdrawal so late — such as a horse refusing to enter the stalls — that no fresh market can be formed.

No. If you backed a horse ante-post and another runner is later withdrawn, your bet stands at the original price with no deduction. If your own horse is the non-runner, though, an ante-post stake is normally lost.

90p in the £. Even if several short-priced runners are withdrawn, the cumulative deduction is capped at 90p, so you always keep at least 10p of every winning pound.

Over 14/1. A horse priced above 14/1 at the time of withdrawal carries no deduction; from 10/1 to 14/1 the deduction is 5p in the £.

Yes — the deduction is applied to both the win return and the place return, so it lands on each part of an each-way bet.

Try the Calculator

Calculate Rule 4 deductions on your winning bet — enter odds, stake, and the withdrawn runner’s price to see exactly how much is taken off your return.

Open the Bet Calculator →